Input Tax Credit refund is one of the most important parts of the GST framework, especially for businesses with high input taxes or regular zero-rated supplies. Many taxpayers in Delhi deal with accumulated ITC because their output liability is lower than the tax paid on inputs. The GST law allows refund of such unutilised credit, but only for specific categories. Understanding who qualifies for an ITC refund helps avoid unnecessary delays, improves cash flow and ensures smooth compliance.

This detailed guide explains every eligible category, conditions to qualify, documentation required, and the process to apply under the GST refund application process. The content aligns with GST rules followed in Delhi and maintains compliance with Google’s content quality guidelines. If you plan to file an ITC refund claim, this guide will help you understand the requirements clearly.

Businesses often pay GST on purchases, raw materials, input services and other business expenses. When the output tax payable is lower than the input tax, the remaining balance stays unused. Over time, this accumulated ITC blocks working capital. The GST framework supports businesses by allowing refunds in certain cases, especially those involving exports, zero-rated supplies and inverted duty structure.

Exporters, manufacturing units, consultancy firms, traders and service providers in Delhi often deal with high levels of ITC accumulation. For them, the GST refund process becomes essential to maintain consistent cash flow. Filing for an ITC refund ensures that the working capital locked in tax credits is released at the right time.

Below are the categories of taxpayers who can legally apply for an ITC refund. These rules follow the CGST Act, SGST Act (Delhi), and relevant notifications issued by GST authorities.

1. Exporters of Goods and Services Without Payment of IGST

Exporters are one of the largest categories eligible for ITC refunds. When businesses export goods or services without paying IGST, they generate accumulated credit on input taxes. Since exports are considered zero-rated supplies, the GST law permits a claim of unutilised ITC.

Exporters in Delhi, including manufacturers and service providers, can apply for a refund under the GST refund on exports category. This includes:

• Export of physical goods

• Export of consultancy or service-based work

• IT/ITES services exported outside India

• Freight and logistics services related to export

Exports without payment of tax fall under Letter of Undertaking (LUT). When the taxpayer exports goods under LUT, they do not pay IGST but can still claim a refund on ITC.

2. Suppliers Facing an Inverted Duty Structure

Businesses that purchase inputs at a higher GST rate and sell finished goods or services at a lower GST rate often face an inverted duty structure. This creates a continuous accumulation of ITC. The law permits refund of the accumulated amount except those restricted under notifications.

Examples include:

• Manufacturers purchasing raw materials at 18% but selling finished goods at 12%

• Service providers paying higher input service tax but billing clients at a lower rate

• Industries where GST rates on raw materials keep changing

Many Delhi-based industries, especially textiles, footwear, chemicals, and certain manufacturing sectors, fall into this category. They can file an ITC refund claim under inverted duty with proper calculations and supporting documents.

3. Supplies Made to SEZ Units or SEZ Developers

Supplies to SEZ (Special Economic Zone) units and developers are treated as zero-rated under GST. If a business supplies goods or services to an SEZ unit without payment of tax, they are eligible to claim a refund of unutilised ITC.

This applies to:

• IT companies located inside SEZs

• Warehousing and logistics units operating from SEZ zones

• Developers building SEZ infrastructure

The supplier must maintain export authorisations, endorsed invoices and SEZ declarations as required under Delhi's GST compliance rules.

4. Deemed Export Supplies

Deemed exports are supplies listed by the government that qualify for export benefit even when the goods do not leave India. Examples include supplies to:

• EOUs (Export Oriented Units)

• Projects funded by the government

• Advance Authorisation holders

• EPCG holders

If the recipient does not claim the refund, the supplier can apply for an ITC refund after fulfilling documentation requirements. Many manufacturing units in Delhi supply to deemed export categories and are eligible for refunds under this provision.

5. Excess Balance in Electronic Cash Ledger

Sometimes taxpayers deposit more money into the cash ledger than required. If the balance remains unused after adjusting tax liability, they can request a refund. This is separate from ITC but processed under the broader category of GST refund services.

Excess cash ledger refunds apply to:

• Wrong tax payment under incorrect head

• Duplicate tax payment

• Payment of tax not required for the period

6. Taxpayers with Finalised Refund Orders After Appeal

If a refund was rejected earlier but later allowed after appeal, the taxpayer qualifies for the approved refund. The refund claim is processed once the order is final and accepted by the GST department.

Businesses must meet certain conditions to qualify for an ITC refund. These conditions are mandatory and followed strictly by GST officers in Delhi.

• ITC must be valid and not fall under blocked credits.

• Supplier must file GSTR-1 and GSTR-3B for the relevant period.

• Invoices must be uploaded correctly, with matching credit in GSTR-2A/2B.

• Exports must have supporting documents such as shipping bills.

• The business must comply with Delhi’s GST rules and maintain correct records.

• No refund is allowed for ITC on capital goods except specific cases.

• If the output supply is exempt or non-taxable, ITC refund is not allowed.

Submitting proper documents reduces the chance of delay or notice from the GST department. The following documents are typically required:

• GSTR-1 and GSTR-3B for the refund period

• Tax invoices and payment proofs

• Statement of inward supplies

• Statement of outward supplies

• LUT for exports without payment of tax

• Shipping bills and export bills

• Bank Realisation Certificates for export services

• Declaration of non-passing of tax burden

• Calculation sheet for inverted duty structure

• Supporting records for SEZ or deemed export supplies

Maintaining accurate documentation is important for a smooth GST refund process.

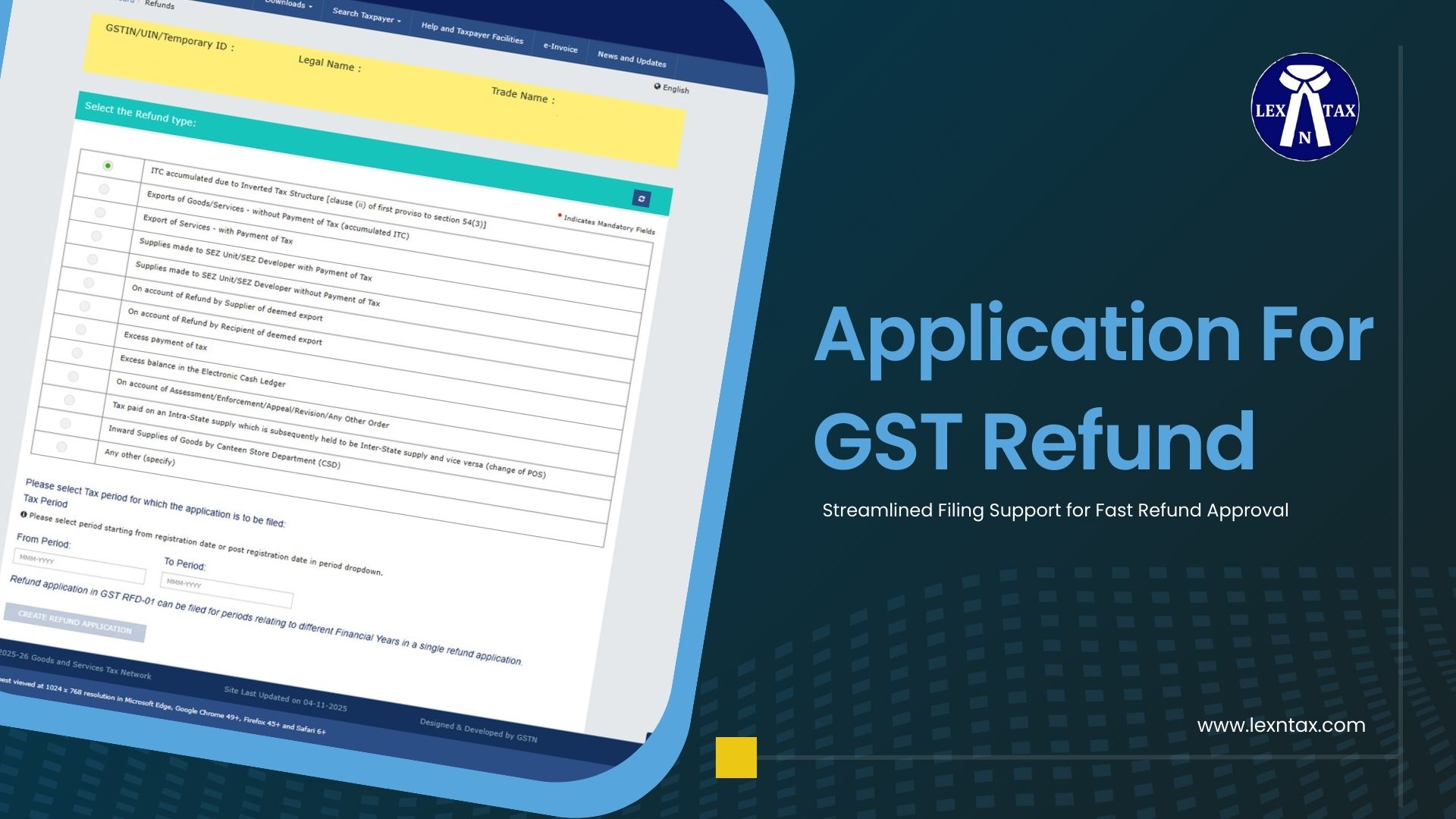

The application is submitted online using Form RFD-01. The main steps include:

Step 1: Login to GST Portal

Navigate to Services → Refunds → Application for Refund.

Step 2: Select Refund Type

Select the appropriate category such as exports, inverted duty or SEZ supplies.

Step 3: Upload Documents

Attach supporting files, statements and declarations.

Step 4: Submit RFD-01

The system generates an ARN for tracking.

Step 5: Verification by GST Officer

The officer checks returns, invoices, documents and eligibility.

Step 6: Refund Order Issued

If everything is correct, RFD-06 (Refund Sanction Order) is issued.

Step 7: Amount Credited

The refund amount is credited to the registered bank account.

The timeline depends on accuracy and compliance. Any mismatch in invoices or documentation causes delays, especially in Delhi where scrutiny standards are high.

Claiming ITC refunds requires careful calculation, document checking and category selection. Errors such as mismatched invoices, wrong refund type or missing proof often lead to delays. Many businesses prefer professional assistance for:

• Correct preparation of refund files

• Avoiding notices and rejections

• Responding to queries from the department

• Faster processing under the GST refund application process

• Compliance with Delhi-specific GST rules

If you need help with filing an ITC refund claim or handling the complete GST refund services, you can contact us for GST Refund Service in Delhi.

1. Who is eligible to claim an ITC refund under GST?

Eligibility is granted to exporters, SEZ suppliers, deemed export suppliers, and businesses operating under inverted duty structure. These groups accumulate unused ITC and can apply for a refund through the GST refund application process.

2. Can a business claim an ITC refund on capital goods?

Generally, refunds on capital goods are not allowed unless specifically notified. Refunds usually apply to inputs and input services.

3. What is the main reason for ITC refund rejections?

Most refunds are rejected due to invoice mismatches, incorrect category selection, and incomplete documentation.

4. How long does the ITC refund process take?

If documents are accurate and returns match, refunds are usually processed within the standard timeline set by GST authorities.

5. Can I get GST refund support in Delhi?

Yes. If you require help with documentation, filing or resolving queries, you can reach out for professional GST Refund Service in Delhi.

6. Who can legally apply for an ITC refund under GST?

Businesses that fall under specific eligible categories can legally apply for an ITC refund. These include exporters of goods and services without payment of IGST, suppliers facing an inverted duty structure, businesses making zero-rated supplies to SEZ units or developers, deemed export suppliers, and taxpayers who have excess balance in their electronic cash ledger. Eligibility depends on compliance with GST rules, filing of correct returns, and maintaining proper documentation.

Finance Minister has announ

In today’s dynamic bu

Lex N Tax Associates offers

Managing income tax filings

International taxation is t

Goods and Services Tax (GST

Income tax is one of the ma

Running a business in India

In a world with a fast-pace

The Goods and Services Tax

Smart tax planning tips for

Taxation and compliance in

In India, the popularity of

In recent years, India has

Filing your Income

In today's fast-paced b

In India's evolving reg

Running a business in Delhi

In today’s business e

In India, MSMEs (Mi

Tax season can be overwhelm

Navigating an incom

Filing income tax in India

Running a business means ju

Exports play a vital role i

For Delhi-based manufacture

For many businesses, especi

Getting a GST refund in Ind

In today’s fast-chang

Updated as per the latest G

The Goods and Services Tax

For many Delhi businesses,

The Goods and Services Tax

The Goods and Services Tax

When it comes to running a

Navigating the GST refund p

The rise of e-commerce in I

Understanding how GST refun

Businesses in India depend

Exporters depend on smooth

Applying for a GST refund i

Understanding who can claim

Goods and Services Tax (GST

Claiming a Goods and Servic

Starting or expanding a bus

Understanding how the GST r

For many businesses in Delh

Businesses in Delhi often f

The GST framework was intro

Maintaining accurate and we

Getting a GST refund on tim

Exporters play a crucial ro

Exporters in Delhi work in

Managing indirect taxes is

Filing an ITC refund on tim

Managing taxes is a routine

Input Tax Credit plays a ce

Input Tax Credit refund is

A Complete Guide fo

Claiming a GST refund can b

Understanding GST R