Understanding GST Refund Laws Applicable in Delhi

Goods and Services Tax refunds play a critical role in maintaining liquidity for businesses operating in Delhi. As a major commercial and trading hub, Delhi has a high volume of GST refund claims arising from exports, inverted duty structures, and excess tax payments. The legal provisions governing GST refunds are uniformly prescribed under central legislation; however, their administration and scrutiny are carried out by the Delhi GST authorities in coordination with the Central GST department.

For Delhi-based taxpayers, understanding both the statutory provisions of the GST law and the procedural expectations followed by Delhi GST officers is essential to ensure smooth processing of refund claims and avoid unnecessary delays or rejections.

The refund mechanism applicable in Delhi is governed by the same statutory framework as applicable across India. These provisions are derived from:

Under this framework, Section 54 of the CGST Act forms the backbone of the GST refund rules in Delhi, laying down the right, eligibility, and limitation period for refund claims. Delhi GST officers administer these provisions in cases where jurisdiction falls under the State tax authority, while certain refunds remain under Central jurisdiction.

Under the GST law applicable in Delhi, a refund refers to the return of tax or other amounts paid in excess or paid incorrectly under the Act. The scope of refund covers several legally recognised situations, including:

The GST refund process ensures that taxpayers in Delhi are not required to bear tax burdens that are not legally payable.

The eligibility criteria for GST refunds in Delhi are governed by Section 54 of the CGST Act read with the Delhi GST Act. To be eligible, the applicant must:

Exporters and suppliers to SEZ units located in or operating from Delhi are specifically protected under the law and are exempt from unjust enrichment provisions.

Understanding GST refund eligibility is particularly important for Delhi traders and service providers who frequently face scrutiny due to high transaction volumes.

The law prescribes a strict limitation period for filing refund claims. A GST refund application must be filed within two years from the relevant date. The determination of the relevant date depends on the nature of the claim.

For Delhi-based taxpayers:

Failure to comply with the GST refund time limit results in irreversible loss of the refund, as Delhi GST authorities do not have discretionary power to condone delay beyond statutory limits.

Refund of accumulated input tax credit is particularly relevant for manufacturers, traders, and service providers in Delhi. Section 54(3) allows refund of unutilised ITC in the following cases:

However, Delhi GST officers closely scrutinise ITC refund claims, especially where rate inversion or classification issues are involved. Refund is not permitted where goods are subject to export duty or where restricted benefits have been availed.

The input tax credit refund provisions must be carefully complied with, as errors in calculation or classification often lead to notices and delayed sanction.

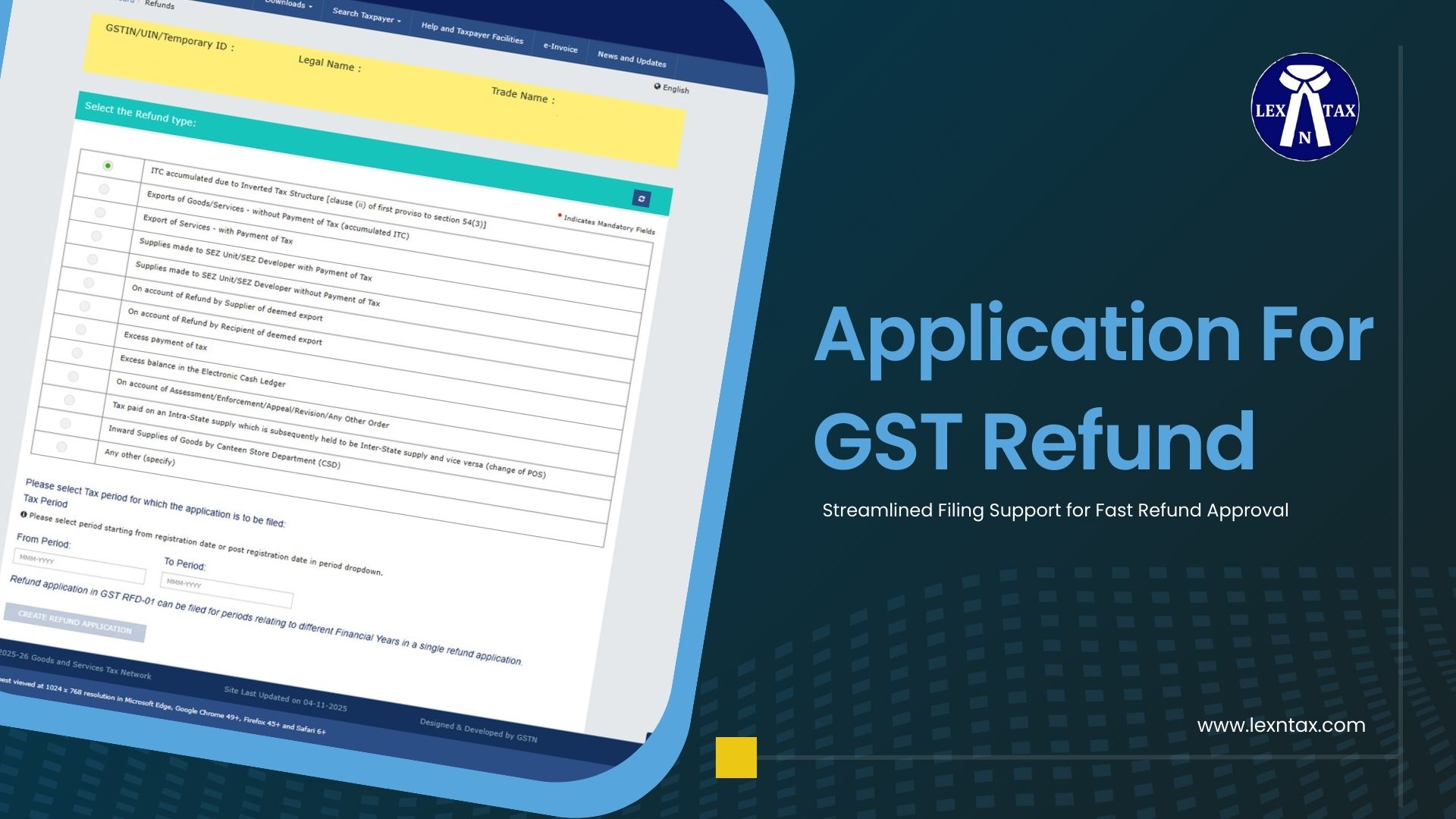

The GST refund application procedure is governed by Rule 89 of the CGST Rules and is common across India. However, Delhi GST authorities are known for detailed verification, particularly in high-value claims.

The process includes:

Incomplete documentation or mismatch in returns such as GSTR-1 and GSTR-3B is a common reason for refund delays in Delhi.

Section 56 of the CGST Act safeguards taxpayers against administrative delays. If a refund is not sanctioned within 60 days from the date of receipt of a complete application, interest becomes payable automatically.

This provision applies equally to refund claims processed by Delhi GST authorities. Interest liability acts as a deterrent against undue delay and reinforces taxpayer confidence in the system.

The doctrine of unjust enrichment ensures that refund benefits reach the person who actually bore the tax burden. Delhi GST officers strictly apply this principle in domestic refund cases.

However, refunds relating to exports, supplies to SEZs, and unutilised ITC are expressly excluded from unjust enrichment requirements. Delhi-based exporters benefit significantly from this statutory protection.

If a refund claim is rejected or sanctioned partially, Delhi taxpayers have the right to file an appeal under the GST appellate framework. Appeals can be filed before the appellate authority having jurisdiction in Delhi within the prescribed time.

Judicial precedents from Delhi High Court have repeatedly held that refund provisions must be interpreted reasonably and that legitimate refunds should not be withheld on technical grounds.

Due to high scrutiny levels, Delhi businesses must ensure strict compliance with refund laws. Proper reconciliation of returns, correct classification of supplies, and timely filing are essential to avoid disputes.

Engaging professional assistance for GST refunds in Delhi helps businesses reduce litigation risk, improve approval timelines, and maintain healthy cash flow.

The legal provisions governing GST refunds provide a strong statutory framework to protect taxpayer rights while safeguarding revenue. For Delhi-based businesses, understanding these provisions and aligning refund claims with both central law and Delhi GST practices is critical.

A well-prepared refund claim, supported by accurate records and legal clarity, ensures timely recovery of funds and long-term compliance under the GST regime.

GST refunds in Delhi are governed by the CGST Act, 2017, the Delhi GST Act, 2017, and the CGST Rules, 2017. Administration depends on jurisdiction between Central and Delhi GST authorities.

A GST refund application must be filed within two years from the relevant date, as defined under Section 54 of the CGST Act. Delay beyond this period results in rejection without condonation.

Yes, Delhi businesses can claim refund of unutilised input tax credit in cases of zero-rated supplies or inverted duty structure, subject to conditions under Section 54(3) of the CGST Act.

Yes. If the refund is not sanctioned within 60 days from the date of receipt of a complete application, interest becomes payable under Section 56 of the CGST Act.

Common reasons include mismatch between GSTR-1 and GSTR-3B, incorrect ITC calculation, incomplete documentation, delayed filing, and non-compliance with unjust enrichment provisions.

Yes. A taxpayer can file an appeal before the GST appellate authority having jurisdiction in Delhi within the prescribed time limit under the GST law.

Finance Minister has announ

In today’s dynamic bu

Lex N Tax Associates offers

Managing income tax filings

International taxation is t

Goods and Services Tax (GST

Income tax is one of the ma

Running a business in India

In a world with a fast-pace

The Goods and Services Tax

Smart tax planning tips for

Taxation and compliance in

In India, the popularity of

In recent years, India has

Filing your Income

In today's fast-paced b

In India's evolving reg

Running a business in Delhi

In today’s business e

In India, MSMEs (Mi

Tax season can be overwhelm

Navigating an incom

Filing income tax in India

Running a business means ju

Exports play a vital role i

For Delhi-based manufacture

For many businesses, especi

Getting a GST refund in Ind

In today’s fast-chang

Updated as per the latest G

The Goods and Services Tax

For many Delhi businesses,

The Goods and Services Tax

The Goods and Services Tax

When it comes to running a

Navigating the GST refund p

The rise of e-commerce in I

Understanding how GST refun

Businesses in India depend

Exporters depend on smooth

Applying for a GST refund i

Understanding who can claim

Goods and Services Tax (GST

Claiming a Goods and Servic

Starting or expanding a bus

Understanding how the GST r

For many businesses in Delh

Businesses in Delhi often f

The GST framework was intro

Maintaining accurate and we

Getting a GST refund on tim

Exporters play a crucial ro

Exporters in Delhi work in

Managing indirect taxes is

Filing an ITC refund on tim

Managing taxes is a routine

Input Tax Credit plays a ce

Input Tax Credit refund is

A Complete Guide fo

Claiming a GST refund can b

Understanding GST R