Claiming a GST refund can be essential for exporters, businesses facing inverted duty structures, and taxpayers who have paid excess tax. This guide explains the current GST refund process in India, step-by-step requirements, important timelines and compliance points — including aspects that are relevant for Delhi-based taxpayers. The content follows Google’s quality standards: original, accurate, and structured for easy reading and search visibility.

Common scenarios where refunds are allowed:

▪ Exporters (zero-rated supplies) claiming refund of unutilized input tax credit (ITC) or IGST paid on exports.

▪ Suppliers to SEZ units or developers (with or without payment of tax).

▪ Tax paid in excess or erroneously.

▪ Refunds arising from assessment, appeals or other specified orders.

▪ Refunds due to inverted duty structure (where tax on inputs > tax on output).

Delhi taxpayers follow the same central GST rules; state processes (for matters coordinated by Delhi trade and taxes department) may add facilitation measures but do not change statutory eligibility under the CGST Act.

▪ Refund claims are governed by Section 54 of the CGST Act and related rules, notably Rule 89 of the CGST Rules (debit to the electronic credit ledger where applicable). Make sure your claim aligns with these provisions.

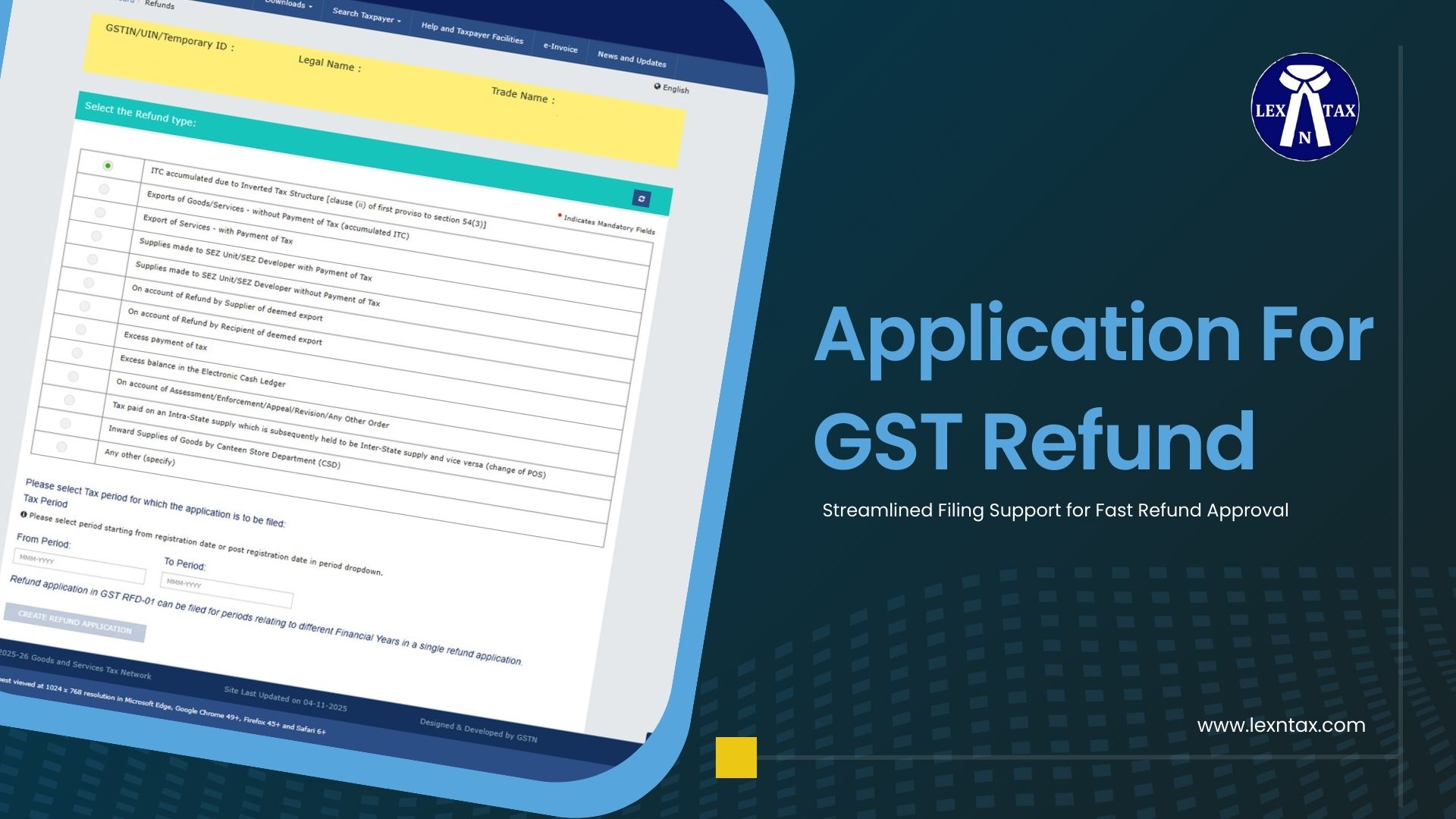

▪ The standard electronic filing medium for refunds is Form GST RFD-01 (filed on the GST portal). Many refund categories must be filed via RFD-01.

▪ Recent CBIC clarifications and circulars (for example, on export-related refunds and post-export price adjustments) affect documentation and the scope of refunds; review relevant circulars when preparing claims.

▪ Determine whether the refund relates to unutilized ITC, excess tax paid, export IGST, assessment/appeal orders, or “any other” ground. Use reconciled returns and ledger balances to compute the claim.

▪ Copy of invoices/exports/shipping bills and bank realization documents (FIRC/BRC) for exports.

▪ Statement of facts and tax ledgers (electronic credit/debit ledger).

▪ Chartered accountant/cost accountant certificate where specified (e.g., for provisional or large claims).

▪ Court/appeal orders if refund follows adjudication.

▪ Any documentation referred to by CBIC circulars for specific categories.

▪ Navigate: Services → Refunds → Application for Refund → RFD-01. Fill the form, select the refund category, and attach the required supporting documents.

▪ After submission, an acknowledgement (RFD-02) is generated. Use Services → Refunds → Track Application Status to monitor progress. Processing involves scrutiny, provisional grants in certain cases, and final orders.

▪ The tax officer may issue notices seeking clarification or additional evidence. Respond promptly through the portal to avoid processing delays.

▪ If the claim is allowed, a refund order (RFD-06 or equivalent) is issued and the amount is paid to the claimant’s bank account linked on the portal. In cases where ITC is refunded, the credit ledger will be debited as per Rule 89.

▪ Limitation period: Generally, a refund application must be filed within two years from the relevant date specified under Section 54. Confirm the exact “relevant date” for your category (export, assessment order, etc.) before filing.

▪ Acknowledgement / provisional payment: The portal typically issues an acknowledgement within a defined period (RFD-02). In specified circumstances, provisional refunds (e.g., RFD-04) can be granted — often subject to safeguards and percentages prescribed by the law or circulars. Check the portal guidance and circulars for current timeframes.

▪ Processing delays & scrutiny: High-value or complex claims may undergo detailed verification, which can extend processing time. Maintain clear documentation and reconcile returns to reduce queries.

▪ GSTIN and bank account details (pre-validated on the GST portal)

▪ Form GST RFD-01 and attachments (invoices, shipping bills, BRC/FIRC for exports)

▪ Reconciled GSTR-1/GSTR-3B data and electronic ledger statements

▪ Chartered accountant/cost accountant certificate (if required)

▪ Copies of assessment/appeal orders, if refund arises from adjudication

▪ Any additional documents requested per circulars (e.g., contract, debit/credit notes)

▪ Reconcile invoices: Ensure invoices on which refund is claimed are correctly reflected in returns (GSTR-1 / GSTR-3B) and the electronic ledgers. Inconsistent data is a leading cause of queries.

▪ Validate bank details: Only the bank account validated on the GST portal will receive refund payments — pre-validate and keep KYC documentation ready.

▪ Use correct refund category: Misclassification leads to procedural confusion and delay. If in doubt, consult GST rules or a tax advisor.

▪ Keep CBIC circulars in view: New clarifications (for example, on post-export price adjustments or documentation) can change document expectations; follow the latest circulars.

Delhi taxpayers follow central GST law for refund eligibility and filing. However, the Delhi Trade & Taxes department may publish state-level orders, policies or facilitation drives (for example, targeted clearance of pending refunds) that affect turnaround times or administrative handling—keep an eye on state notifications and departmental portals for such initiatives. For complex or disputed claims, state trade & taxes orders and communications can be relevant.

▪ Mismatch between claimed invoices and uploaded returns or ledgers.

▪ Missing or non-validated bank details.

▪ Incomplete supporting documentation (especially for exports — shipping bills, FIRC/BRC).

▪ Claim outside limitation period (beyond two years).

▪ Inconsistent valuation or tax treatment leading to officer scrutiny.

If your refund claim involves large amounts, complex cross-border transactions, post-export price adjustments, or appeals and court orders, engage a tax professional with GST refund experience. They can help prepare CA certificates, reconcile ledgers, and represent you during departmental queries — useful for ensuring compliance with both CBIC circulars and Rule 89 requirements.

Q: Which form is used to apply for a refund?

A: Form GST RFD-01 (filed on the common GST portal) for most refund categories.

Q: How long do I have to file a refund claim?

A: Usually within two years from the relevant date under Section 54, subject to category-specific rules.

Q: Can I claim refund of unutilized ITC for exports?

A: Yes — unutilized ITC on account of zero-rated supplies can be claimed via RFD-01 following prescribed conditions.

The GST refund process in India is well-defined but document-sensitive. Filing an accurate RFD-01 with reconciled returns and complete supporting evidence is the single best step toward a smooth refund. For Delhi taxpayers, central rules apply, while state notifications may influence processing speed and administrative support. If the claim is sizable or complex, consider professional assistance to avoid avoidable delays.

Finance Minister has announ

In today’s dynamic bu

Lex N Tax Associates offers

Managing income tax filings

International taxation is t

Goods and Services Tax (GST

Income tax is one of the ma

Running a business in India

In a world with a fast-pace

The Goods and Services Tax

Smart tax planning tips for

Taxation and compliance in

In India, the popularity of

In recent years, India has

Filing your Income

In today's fast-paced b

In India's evolving reg

Running a business in Delhi

In today’s business e

In India, MSMEs (Mi

Tax season can be overwhelm

Navigating an incom

Filing income tax in India

Running a business means ju

Exports play a vital role i

For Delhi-based manufacture

For many businesses, especi

Getting a GST refund in Ind

In today’s fast-chang

Updated as per the latest G

The Goods and Services Tax

For many Delhi businesses,

The Goods and Services Tax

The Goods and Services Tax

When it comes to running a

Navigating the GST refund p

The rise of e-commerce in I

Understanding how GST refun

Businesses in India depend

Exporters depend on smooth

Applying for a GST refund i

Understanding who can claim

Goods and Services Tax (GST

Claiming a Goods and Servic

Starting or expanding a bus

Understanding how the GST r

For many businesses in Delh

Businesses in Delhi often f

The GST framework was intro

Maintaining accurate and we

Getting a GST refund on tim

Exporters play a crucial ro

Exporters in Delhi work in

Managing indirect taxes is

Filing an ITC refund on tim

Managing taxes is a routine

Input Tax Credit plays a ce

Input Tax Credit refund is

A Complete Guide fo

Claiming a GST refund can b

Understanding GST R