International taxation is the branch of tax law that deals with the tax implications of cross-border transactions and activities. It encompasses the rules and regulations that govern how countries tax individuals, businesses, and transactions that occur across national borders.

Key principles of international taxation include residence-based taxation, where individuals and businesses are taxed based on their residency status, and source-based taxation, where income is taxed in the country where it is earned. Double taxation, which occurs when the same income is taxed by more than one country, is a significant concern in international taxation. To mitigate this, countries often negotiate tax treaties that allocate taxing rights and provide mechanisms to relieve double taxation.

International taxation plays a critical role in today’s globalized economy, where businesses and individuals often operate across multiple jurisdictions. As companies expand internationally and digital services become borderless, understanding international tax rules becomes increasingly important for maintaining compliance and avoiding legal pitfalls.

The global nature of commerce means income can be earned in one country, managed in another, and taxed in both. Without clear international tax rules, this would lead to confusion, excessive tax burdens, and potential tax evasion.

International taxation ensures that:

Governments can fairly collect tax on income earned within their borders.

Taxpayers are not unfairly taxed multiple times on the same income.

Multinational companies follow consistent standards when reporting income.

These principles help create a more balanced and predictable global tax environment, which is essential for economic growth and foreign investment.

1. Tax Residency

A central concept in international taxation is tax residency. An individual or business may be considered a tax resident of a country based on several factors such as:

Place of incorporation (for companies)

Physical presence or domicile (for individuals)

Central management and control

Tax residency determines which country has the right to tax worldwide income.

2. Source of Income

The source of income refers to the country where the income originates. For example, if a company in India provides services to a client in the US, the source of income could be the US. Source-based taxation allows countries to tax income generated within their borders, regardless of the taxpayer’s residency.

3. Double Taxation

Double taxation occurs when the same income is taxed by two different countries. This can happen when both the country of residence and the country of source claim taxing rights. To resolve this, many countries enter into Double Taxation Avoidance Agreements (DTAAs).

Tax treaties or DTAAs are bilateral agreements between countries that aim to avoid or mitigate double taxation. These treaties typically:

Define which country has the right to tax specific types of income (e.g., dividends, royalties, business income)

Provide mechanisms for tax relief such as tax credits or exemptions

Outline procedures for resolving tax disputes through mutual agreement

For example, under a DTAA between India and the UK, a UK resident earning income in India may be eligible for tax relief in the UK for taxes paid in India, reducing the overall tax burden.

Multinational companies often shift profits across borders to take advantage of lower tax rates. To prevent this, tax authorities enforce transfer pricing rules. Transfer pricing ensures that transactions between related entities (e.g., parent and subsidiary) are priced fairly — as if they were between independent parties.

Additionally, the OECD’s Base Erosion and Profit Shifting (BEPS) initiative has introduced global standards to prevent tax avoidance through artificial profit shifting. These measures promote transparency, substance-based taxation, and equitable tax practices among nations.

The rise of digital businesses — such as streaming platforms, online marketplaces, and software-as-a-service (SaaS) providers — has created new challenges in international taxation. Many digital companies earn significant revenue in countries where they have no physical presence. As a result, tax authorities are pushing for new frameworks that allow for digital taxation, including:

Significant economic presence rules

Equalization levies

Global minimum tax (under OECD Pillar Two)

For businesses, especially startups and multinationals, international tax compliance is vital to avoid audits, penalties, and reputational risks. Hiring tax professionals or international tax consultants can ensure:

Proper tax structuring

Effective use of tax treaties

Timely reporting and compliance with foreign tax laws

For individuals, especially expatriates or those earning foreign income, understanding residency rules, foreign tax credits, and treaty benefits is crucial for accurate tax filing.

International taxation is not just a niche legal area — it’s a cornerstone of global business and economic policy. With changing tax laws, evolving digital models, and increased international cooperation, staying informed about international tax regulations is more important than ever.

Whether you're a business owner, a tax consultant, or an individual with cross-border income, understanding the principles of international taxation helps you stay compliant and make smart financial decisions in the global marketplace.

Finance Minister has announ

In today’s dynamic bu

Lex N Tax Associates offers

Managing income tax filings

International taxation is t

Goods and Services Tax (GST

Income tax is one of the ma

Running a business in India

In a world with a fast-pace

The Goods and Services Tax

Smart tax planning tips for

Taxation and compliance in

In India, the popularity of

In recent years, India has

Filing your Income

In today's fast-paced b

In India's evolving reg

Running a business in Delhi

In today’s business e

In India, MSMEs (Mi

Tax season can be overwhelm

Navigating an incom

Filing income tax in India

Running a business means ju

Exports play a vital role i

For Delhi-based manufacture

For many businesses, especi

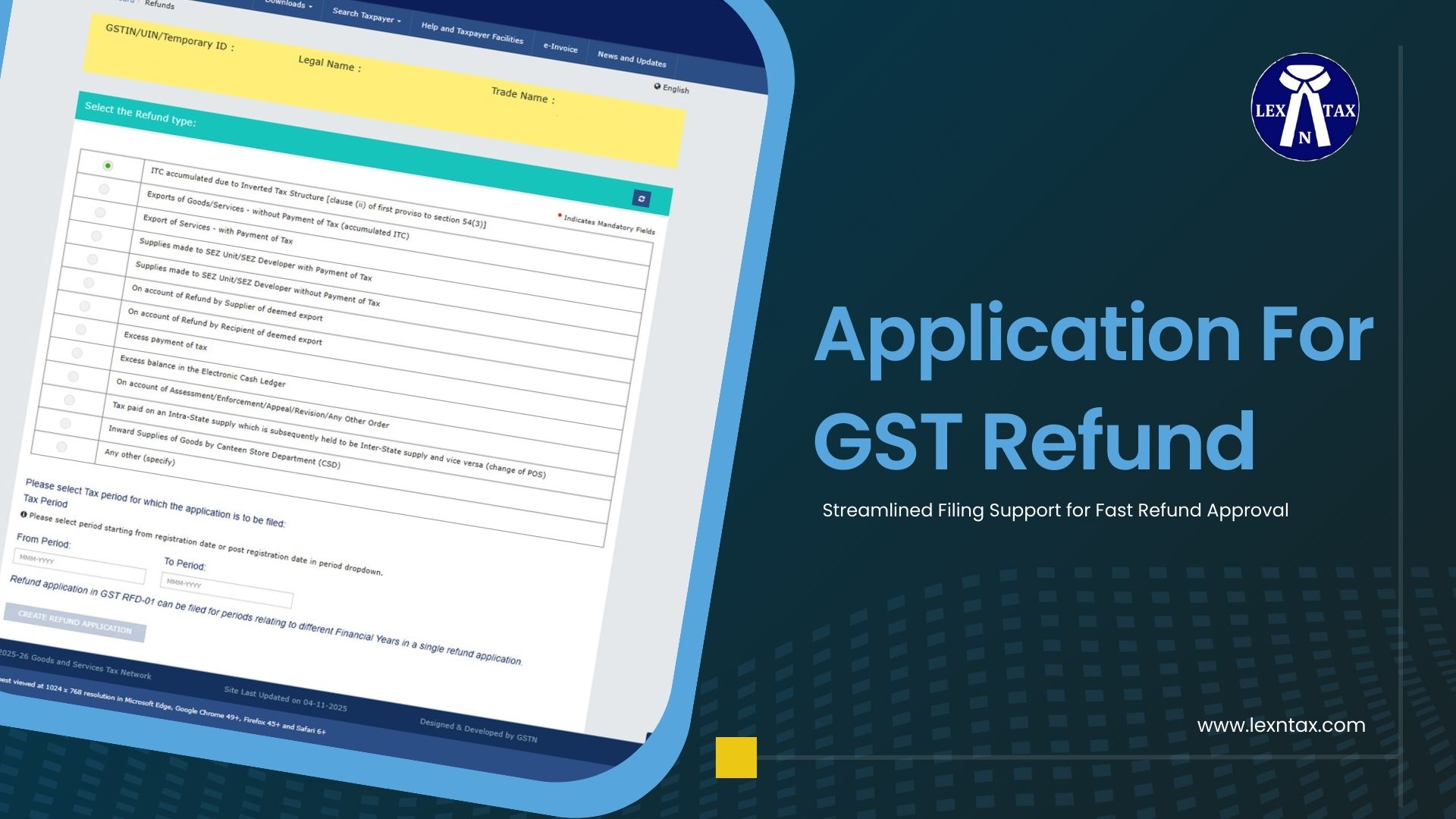

Getting a GST refund in Ind

In today’s fast-chang

Updated as per the latest G

The Goods and Services Tax

For many Delhi businesses,

The Goods and Services Tax

The Goods and Services Tax

When it comes to running a

Navigating the GST refund p

The rise of e-commerce in I

Understanding how GST refun

Businesses in India depend

Exporters depend on smooth

Applying for a GST refund i

Understanding who can claim

Goods and Services Tax (GST

Claiming a Goods and Servic

Starting or expanding a bus

Understanding how the GST r

For many businesses in Delh

Businesses in Delhi often f

The GST framework was intro

Maintaining accurate and we

Getting a GST refund on tim

Exporters play a crucial ro

Exporters in Delhi work in

Managing indirect taxes is

Filing an ITC refund on tim

Managing taxes is a routine

Input Tax Credit plays a ce

Input Tax Credit refund is

A Complete Guide fo

Claiming a GST refund can b

Understanding GST R